Below are some interesting charts which I picked up in this Zerohedge article.

First, the phenomena which got the problem countries into trouble in the first place - current account deficits: Greece & Co. had been spending much more money outside their borders than they had revenues outside their borders, having to cover the gap with loans from outside their borders. Today, 8 years later, the situation is as follows:

There are current account surpluses wherever one looks. Almost wherever one looks: France seems to have become rather problematic with a current account deficit representing almost 4% of GDP but Greece's current account deficit is now minute compared to what it used to be.

A current account surplus doesn't mean that the domestic economy is in order. All it means is that the country is financially self-supporting as regards its economic activities outside its borders. It has enough revenues outside its borders to pay for all the essential and non-essential imports the country is buying. Theoretically, the country could be barred from any foreign credit and yet, it could continue its cross-border transactions.

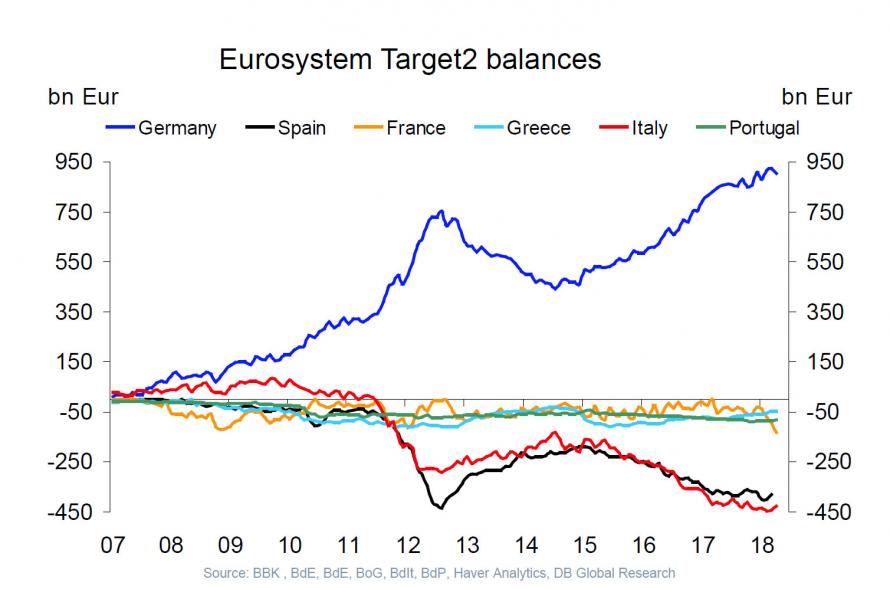

The next chart is particularly interesting. The credible narrative had been that the ECB's Target2 payment system - as a quasi unlimited credit card - allowed countries to run current account deficits even though the foreign private banks were no longer funding them. That was certainly true in the early years but following that logic and seeing current account surpluses now, one would expect Target2 claims of the North to decline.

The following chart shows the development of the (in)famous Target2 balances:

The earlier narrative no longer holds because Target2 claims of the North, specifically of Germany, have increased phenomenally even though current account surpluses were recorded in most countries. There is only one other explanation: capital flight. Now here is something to ponder for all those who always blame Germany for bleeding out the suffering South: Germany has run up nearly a trillion Euros worth of Target2 claims so that, mostly, Italy and Spain could transfer money out of their countries (even back to Germany). Should Italy or Spain ever exit the Eurozone, the Bundesbank might say to them "We want you to give us our money back" and Italy or Spain would respond "The money is already back in your banking system, except it's now in our name and no longer in yours!"

Much has been said about the brutal internal devaluations which the South has had to go through. No doubt that's true for Greece but when one looks at Italy, one sees that nominal unit labor costs, the most crucial element of international competitiveness, have actually increased by 10% since the crisis began. The new Italian government intends to increase deficit spending which is unlikely to favorably impact nominal unit labor costs.

And now to the final chart which leads J. P. Morgan to the conclusion that an exit from the Eurozone may be Italy's best option:

Italy's net foreign investment position is only minimally negative which leads J. P. Morgan to conclude that an Italian Euro exit should be a lot less threatening to creditors than a Spanish one. Put differently, with a current account surplus and a walk-away from Target2 liabilities, Italy would owe only very little to foreigners. Well, not quite because the above foreign investment position is a net between assets and liabilities. While the assets/liabilities are not necessarily owned/owed by the same parties, it is still a fact that there are about 3 trillion Euros of Italian financial assets outside the country's borders and foreign creditors would use all legal expertise to get a hold of some of them.

The old saying goes "If you owe the bank 100.000 Euros, you have to be nervous. If you owe the bank 100 million Euros, the bank has to be nervous." Germany has many more reasons to be nervous about an Italian exit from the Eurozone than Italy itself. And here is another thought.

Deutsche Bank, once Germany's financial calling card, is in great difficulties. Should Germany ever be called upon to bail-out Deutsche Bank, they will discover that Deutsche Bank is counter-party in derivatives with a notional amount totalling almost 3 times the GDP of the United States!

Certainly at that point, Germany will stop educating others about reforming their financial sectors and economies.

First, the phenomena which got the problem countries into trouble in the first place - current account deficits: Greece & Co. had been spending much more money outside their borders than they had revenues outside their borders, having to cover the gap with loans from outside their borders. Today, 8 years later, the situation is as follows:

There are current account surpluses wherever one looks. Almost wherever one looks: France seems to have become rather problematic with a current account deficit representing almost 4% of GDP but Greece's current account deficit is now minute compared to what it used to be.

A current account surplus doesn't mean that the domestic economy is in order. All it means is that the country is financially self-supporting as regards its economic activities outside its borders. It has enough revenues outside its borders to pay for all the essential and non-essential imports the country is buying. Theoretically, the country could be barred from any foreign credit and yet, it could continue its cross-border transactions.

The next chart is particularly interesting. The credible narrative had been that the ECB's Target2 payment system - as a quasi unlimited credit card - allowed countries to run current account deficits even though the foreign private banks were no longer funding them. That was certainly true in the early years but following that logic and seeing current account surpluses now, one would expect Target2 claims of the North to decline.

The following chart shows the development of the (in)famous Target2 balances:

Much has been said about the brutal internal devaluations which the South has had to go through. No doubt that's true for Greece but when one looks at Italy, one sees that nominal unit labor costs, the most crucial element of international competitiveness, have actually increased by 10% since the crisis began. The new Italian government intends to increase deficit spending which is unlikely to favorably impact nominal unit labor costs.

And now to the final chart which leads J. P. Morgan to the conclusion that an exit from the Eurozone may be Italy's best option:

Italy's net foreign investment position is only minimally negative which leads J. P. Morgan to conclude that an Italian Euro exit should be a lot less threatening to creditors than a Spanish one. Put differently, with a current account surplus and a walk-away from Target2 liabilities, Italy would owe only very little to foreigners. Well, not quite because the above foreign investment position is a net between assets and liabilities. While the assets/liabilities are not necessarily owned/owed by the same parties, it is still a fact that there are about 3 trillion Euros of Italian financial assets outside the country's borders and foreign creditors would use all legal expertise to get a hold of some of them.

The old saying goes "If you owe the bank 100.000 Euros, you have to be nervous. If you owe the bank 100 million Euros, the bank has to be nervous." Germany has many more reasons to be nervous about an Italian exit from the Eurozone than Italy itself. And here is another thought.

Deutsche Bank, once Germany's financial calling card, is in great difficulties. Should Germany ever be called upon to bail-out Deutsche Bank, they will discover that Deutsche Bank is counter-party in derivatives with a notional amount totalling almost 3 times the GDP of the United States!

Certainly at that point, Germany will stop educating others about reforming their financial sectors and economies.

I have great difficulties...

ReplyDeleteYou have great difficulties...

he;she;it has great difficulties..

we have great difficulties...

you have great difficulties...

they have great difficulties...

Ok! The Breakup Blues: It's Over!

Yes, We have read it in Spiegel and Handesblatt

Ohhh!!!

Dear Germans (http://www.cambridge.org/gb/academic/subjects/history/european-history-after-1450/origins-nationalism-alternative-history-ancient-rome-early-modern-germany?format=PB)

We understand you, but...

"Fight the Problem, not the Person"

What would be your reply, Stavros, if we opted out of the initially purely economic and then later idealist project the EEC/EU? Never mind the devil always lies in the details on the respective unifying ground as far as idealist projects are concerned?

DeleteE.g. what if we followed the Swiss option? Strictly, that would have been my favorite choice with 18. No rearmament beyond protection. How comes the subject has shifted to the right? For this elder this feels a bit odd. We only have to protect our borders concerning the "have nots" or driven away by war and struggles. ...

Back to my above question, assuming we opted out, would we be a lesser or even bigger threat? You tell me? If the lesser, why don't you opt for Germany to leave the European union? From a group? Propose it?

The rest of Europe would find a way to accommodate once the obstructionist Germans are out?

Could you give me a nutshell of why you alert to Capar Hirschi's publication? Maybe I misunderstood. For what it is worth, I was highly interested in nationalism from early on. My favorite in the field is Roger Griffin.

Anyway, I'll check reviews. Starting with this one.

LeaNder

http://www.history.ac.uk/reviews/review/1281

LeaNder

Dear Stavros,

Deleteseems Google is targeting me lately among others, on the surface it looked as if it was Google. They even may be making it past my usual Firewalls. Resulting in oddities like Roger Griffin showing up in my usual search routine in my favorite University Library. Without me even entering a search term, that is. ...

On the other hand seriously no library ever bought a copy of this publication?

https://www.amazon.com/Russian-1920-1941-Oxford-Historical-Monographs/dp/0199250219

You still owe me an answer, why as German, after all you address us collectively--"Dear Germans"--this is a must-read-book for me or us considered collectively?

LeaNder

LeaNder

At Some Point Germans May Discover That They Are In Deep Trouble

ReplyDeleteI have been aware for a long time. ...

LeaNder

If the Germans sweat so much over Target2, why don't they send the money back to where they came from? Reducing their absurdly large current-account surplus would be such a way. That would also work as a fine recycling mechanism.

ReplyDeletekleingut, about Vollgeld initiative how logical it is?

ReplyDeletehttps://www.vollgeld-initiative.ch/english/

From the little I know about Vollgeld, it sounds to me very much like a 'planned' financial system, i. e. the Central Bank determines how much money/credit the real economy needs. But I may be wrong. I think there are better ways to stabilize the financial system, the best one I have heard so far comes from the former governor of the Bank of England, Mervyn King.

ReplyDeleteKing proposes that banks should be required to have committed back-up lines from their respective Central Banks in the amount of their total liabilities up to 1 year. The Central Banks would require the banks to post enough eligible collateral as security for this line (similar to ELA, except it would have to be worthy collateral and not Greek bonds). That in itself would constrain banks in their expansion because they may not have sufficient eligible collateral.

The point of this is that there cannot be a bank run and/or liquidity crisis of a bank: the bank's liquidity is safe for up to 1 year, and 1 year is enough time either to solve the bank's problems (if they can be solved) or to arrange an orderly liquidation.

Add to that a reasonably conservative total leverage ratio (total liabilities to equity), say 5:1, and the banking system is totally stable.

Thank you for the comment.

ReplyDeleteIn "The End of Alchemy" Mervyn King is writing about the definition of "good collateral" and Walter Bagehot in the crisis of 1866 (lender of last resort)

"Banks are very different from banks in Bagehot’s time (...) They are bigger, their assets are more complex and difficult to value, they hold far fewer liquid assets, they finance themselves with far less equity capital, and they wield greater political power.

As a result, the maxim ‘lend freely against good collateral at a penalty rate’ is outdated (Bagehot approach) ."

(...)"Until well into the post-war period, banks

held around 30 per cent of their assets in the form of government securities,most of them short-term and all of them liquid."

What i can't understand is the motive for someone with deposit 1 mln CHF to "give" (the bank) a loan to someone with 10.000 CHF deposit, even with good collateral, if we accept that banks generally hold far fewer liquid assets even at 1% in total.

Its like a closed box.

Typically, in the initiative claim that 90% is electronic money and only 10% in circulation, so it is easy to find lines of credit for that 10%.

This is probably a very complex issue, and my approach may be a general reference or simplification that does not touch the core of the issue.

Mervyn King's approach about back up lines up to a year is related with the initiative approach or is independent and is implemented under current banking rules?

It seems logical.

King's proposal is totally unrelated to the Vollgeld Initiative. He wrote a book after leaving office; he obviously intended to make historical proposals in that book and the result was the above proposal. One can obviously raise the question whether Central Banks can be efficient administrators of collateral appraisal, valuation, etc. etc. But the ECB is doing it already with ELA.

DeleteSorry, Klaus for my unrelated diatribe above.

DeleteI get emotional sometimes, I wish I didn't, but yes lately I seem to respond like a Pavlovian Dog, here too. ...

Concerning my second comment. I am beyond relaxing on the idea of being a nobody in this brave new universe. ...

LeaNder

Dear Klaus Kastner, I am not necessarily a fan of The Saker, but admittedly I found Pepe Escobar an interesting voice in the early post 9/11 universe. And yes strictly on the blog I follow there was an early reference to Syria from someone I find one of the more, although more rare too, contributors. At one point in time he mentioned in the comment section that China may be poised (?) to help rebuilding in Syria. The Piraeus Port port surfaces too in passing in Escobar's narrative. We stumbled across it here too. The interview shifts to English after a while.

ReplyDeleteStrictly China, always take my comments with a grain of salt, but China too seems to have his own inner Turkmen problem. As Russia. Chechnya? Some Turkmen were rumored to fight in Syria. ...

http://thesaker.is/interview-of-pepe-escobar-the-world-is-waiting-for-the-apocalypse-if-there-is-a-conflict-between-america-and-russia/

Glass Seagall?

http://turcopolier.typepad.com/sic_semper_tyrannis/2018/06/harper-happy-anniversary-glass-steagall-we-miss-you-come-back.html

Strictly, I have to admit, Trump's approach sounds like a variation of the old trickle down theory. Some more polite ennobled members in the leverage investment camp seem to have come to the conclusion it may not work anymore quite a while ago.

LeaNder, the nitwit babbler